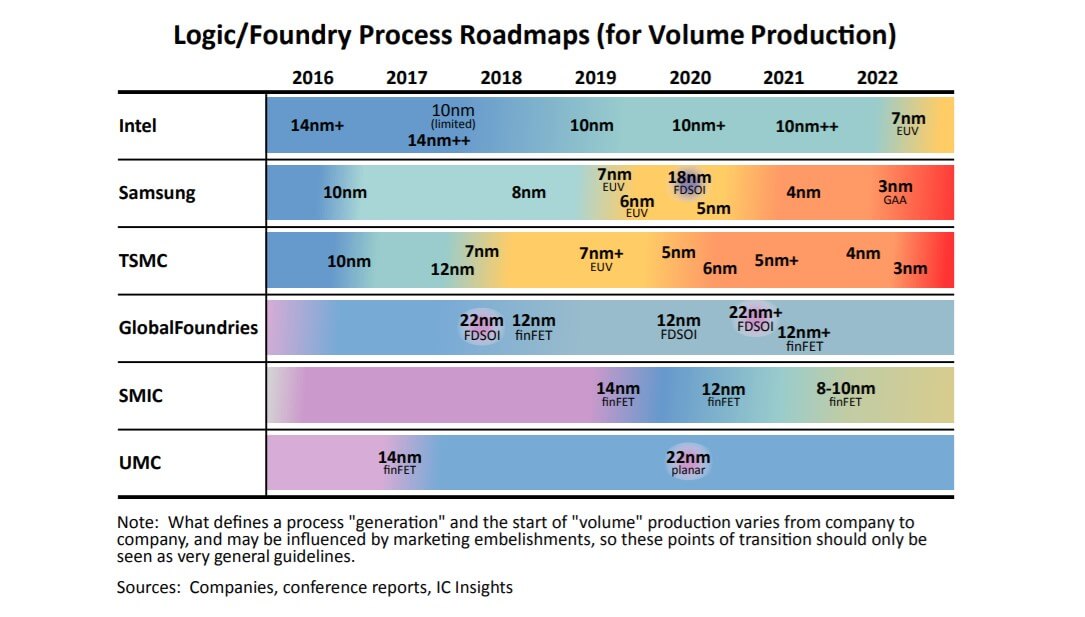

According to the data provided in the latest report released by IC Insights, many fabless IC companies are clamoring to have their leading-edge devices, including high-performance microprocessors, low-power application processors, and other advanced logic devices, fabricated using 7nm and 5nm process nodes. Some of the current iterations from logic and foundry suppliers are shown in the figure below.

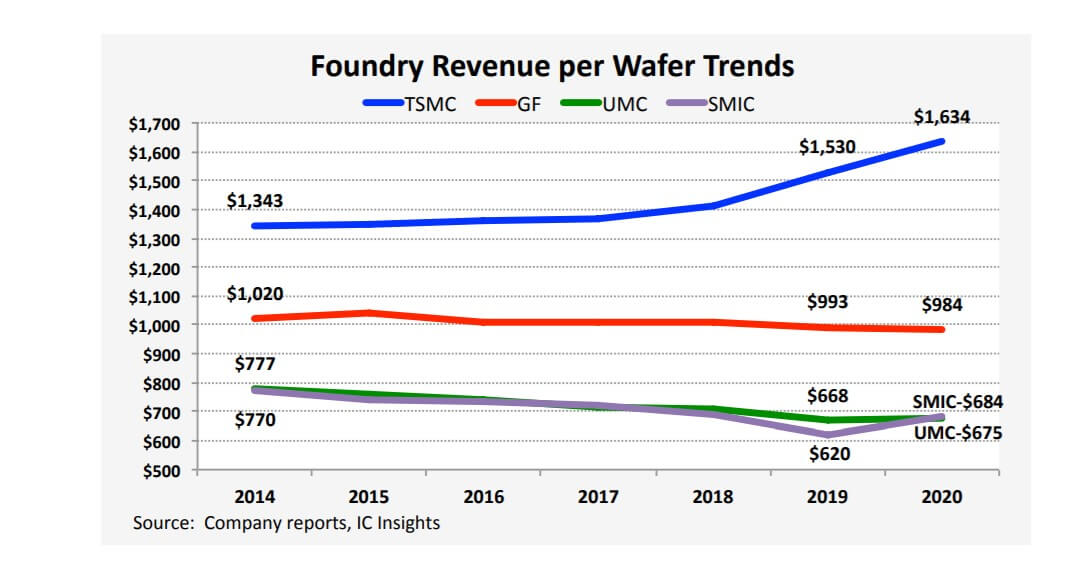

IC Insights pointed out in the report that, especially in the foundry world, manufacturing with leading-edge processes carries a distinct advantage. In 2020, TSMC was the only pure-play foundry manufacturing ICs using both 7nm and 5nm process nodes. Not coincidentally, its overall revenue per wafer increased significantly in 2020 as many of the top fabless IC suppliers—16 fabless IC companies with more than $1.0 billion in 2020 revenue—lined up to have their newest designs manufactured using these most advanced processes. Three of the four pureplay foundries enjoyed higher revenue-per-wafer in 2020 (GlobalFoundries’ revenue per wafer slipped 1% last year). TSMC’s figure of $1,634 exceeded GlobalFoundries by 66% and was more than double the revenue per wafer value at UMC and SMIC. With estimated capital expenditures of $27.5 billion in 2021, TSMC will expand its available capacity at these nodes and also begin risk production of 3nm ICs this year with volume production slated to start in 2022.

The report said that besides foundry and logic IC manufacturing, memory suppliers like Samsung, Micron, SK Hynix, and Kioxia/WD are using advanced processes to make their DRAM and flash memory components. No matter the device type, the IC industry has evolved to the point where only a very small group of companies can develop leading-edge process technologies and fabricate leading edge ICs.

At the end of the report, IC Insights pointed out that with the increase in the share held by top manufacturers, the market share composition of each IC product field has become "top heavy", leaving little room for remaining competitors.

All Comments (0)