March 4, 2026 /SemiMedia/ — Global NAND Flash revenue climbed sharply in the fourth quarter of 2025, helped by strong demand from AI infrastructure projects, according to TrendForce.

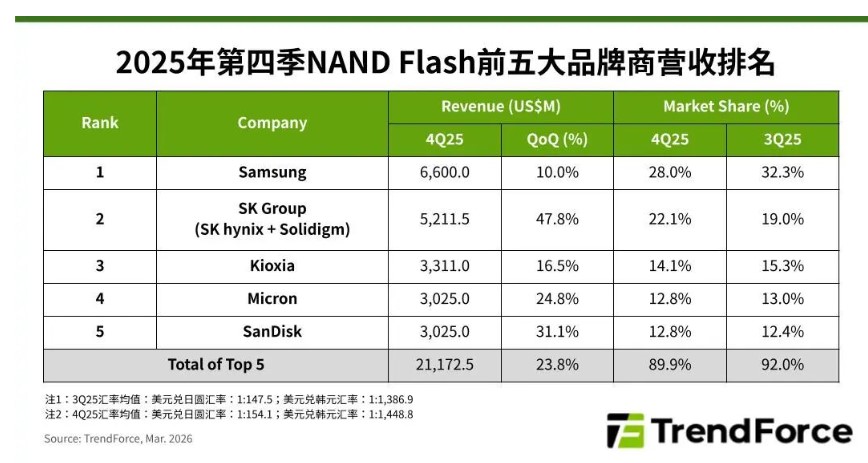

The research firm said combined revenue of the top five suppliers reached $21.17 billion in the quarter, up 23.8% from the previous period.

Looking ahead to the first quarter of 2026, TrendForce expects tight supply to keep pushing prices higher. The firm raised its forecast for average NAND Flash contract prices to grow about 85% to 90% quarter on quarter, which should support further revenue gains.

By vendor, Samsung remained the largest supplier with revenue of $6.6 billion, up 10% sequentially, though its market share slipped to 28%. The SK Group, including SK hynix and Solidigm, posted the fastest growth, with revenue rising 47.8% to $5.21 billion. Its share increased to 22.1%, supported by stronger shipments of mobile NAND and enterprise SSD products.

Kioxia ranked third with revenue of $3.31 billion, up 16.5% from the prior quarter, reaching a new quarterly high in both revenue and bit shipments. Micron came fourth with revenue of about $3.03 billion, up 24.8%. The company is expanding QLC output and ramping products based on its ninth-generation (G9) NAND technology to drive bit growth in 2026. SanDisk followed in fifth place with revenue also near $3.03 billion, rising 31.1% sequentially.

TrendForce said NAND Flash prices are likely to stay elevated through 2026, as capacity expansion remains limited while AI-related demand continues to grow.

All Comments (0)