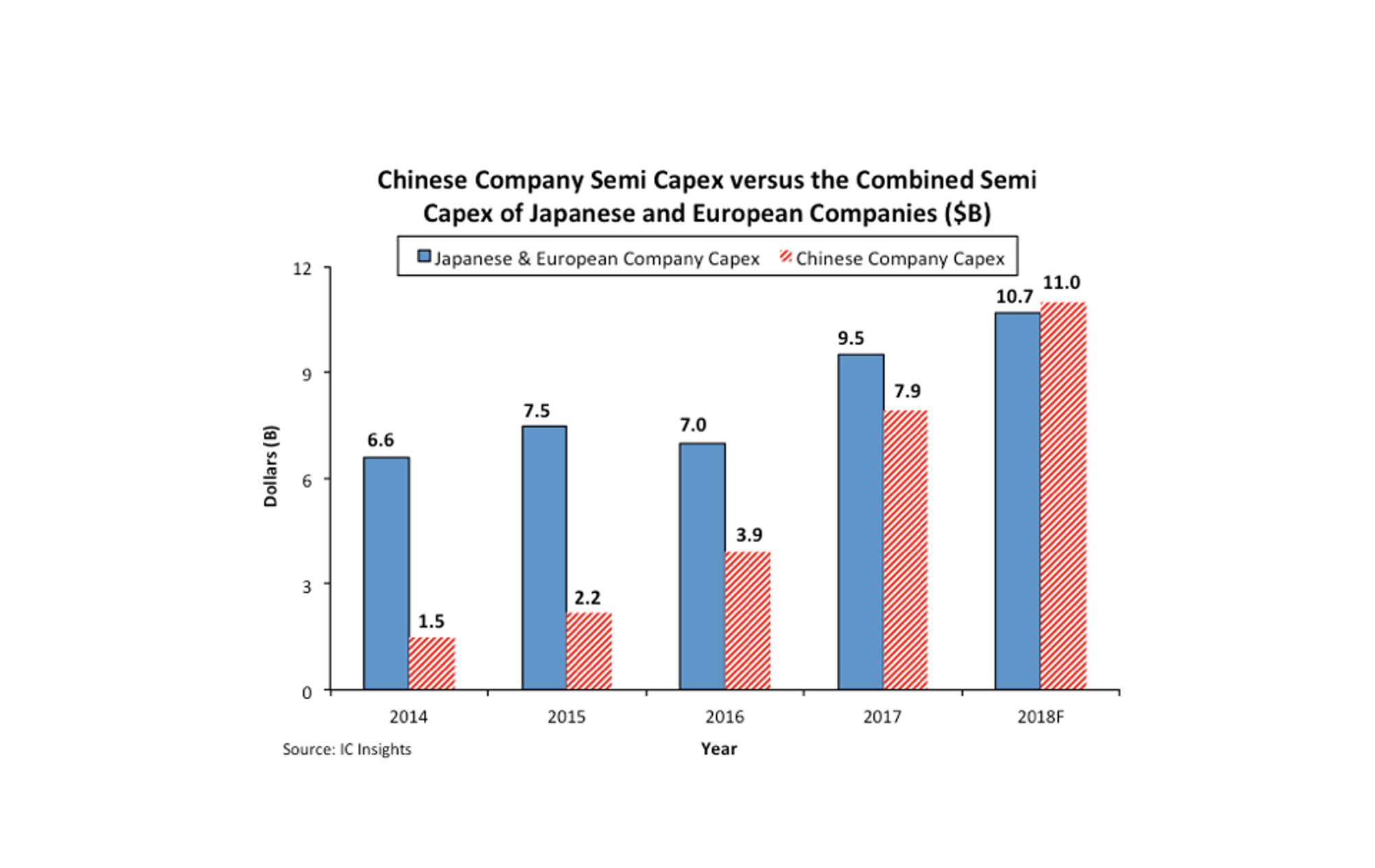

According to data from IC Insights, China’s semiconductor company’s capital expenditure this year will reach US$11 billion, this data in 2015 was US$2.2 billion.

As shown in the above chart, IC Insights predicts that China’s semiconductor company’s capital expenditures in 2018 will reach US$11 billion, which will be 10.6% of the expected global expenditure of US$103.5 billion. This is not only five times the total expenditure of China Semiconductor in 2015, but also exceeds the sum of capital expenditure of Japanese and European semiconductor companies this year.

Due to the adoption of the FAB-lite business model, the capital expenditures of the semiconductor giants in Europe this year accounted for only 4% of global spending. Although European companies’ semiconductor spending will surge from time to time, such as the surge in spending of ST and AMS in 2017, IC Insights believes that European companies’ global semiconductor spending in 2022 will only account for 3% of the world's total.

It is worth noting that some Japanese semiconductor companies have gradually transformed into fab-lite business models (such as Renesas, Sony, etc.). In fact, Japanese companies are expected to account for only 6% of the capital expenditure of the global semiconductor industry in 2018, it was 51% in 1990, and 22% in 2005. In the past 20 years, Japan’s global semiconductor spending has been declining.

Although the Chinese-based foundry SMIC has long been a major investment target for the semiconductor industry, another four Chinese companies are expected to become important investment targets for the semiconductor industry this year. They are YMTC, Innotron, JHICC and Shanghai Huali. There is no doubt that China’s spending and development in the semiconductor industry have both increased in recent years. In the next 10 years, China will play an increasingly important role in the global semiconductor landscape.

For more information please visit: http://www.icinsights.com/news/bulletins/Chinas-Semi-Capex-Forecast-To-Be-Larger-Than-Europe-And-Japan-Combined-In-2018/

All Comments (0)