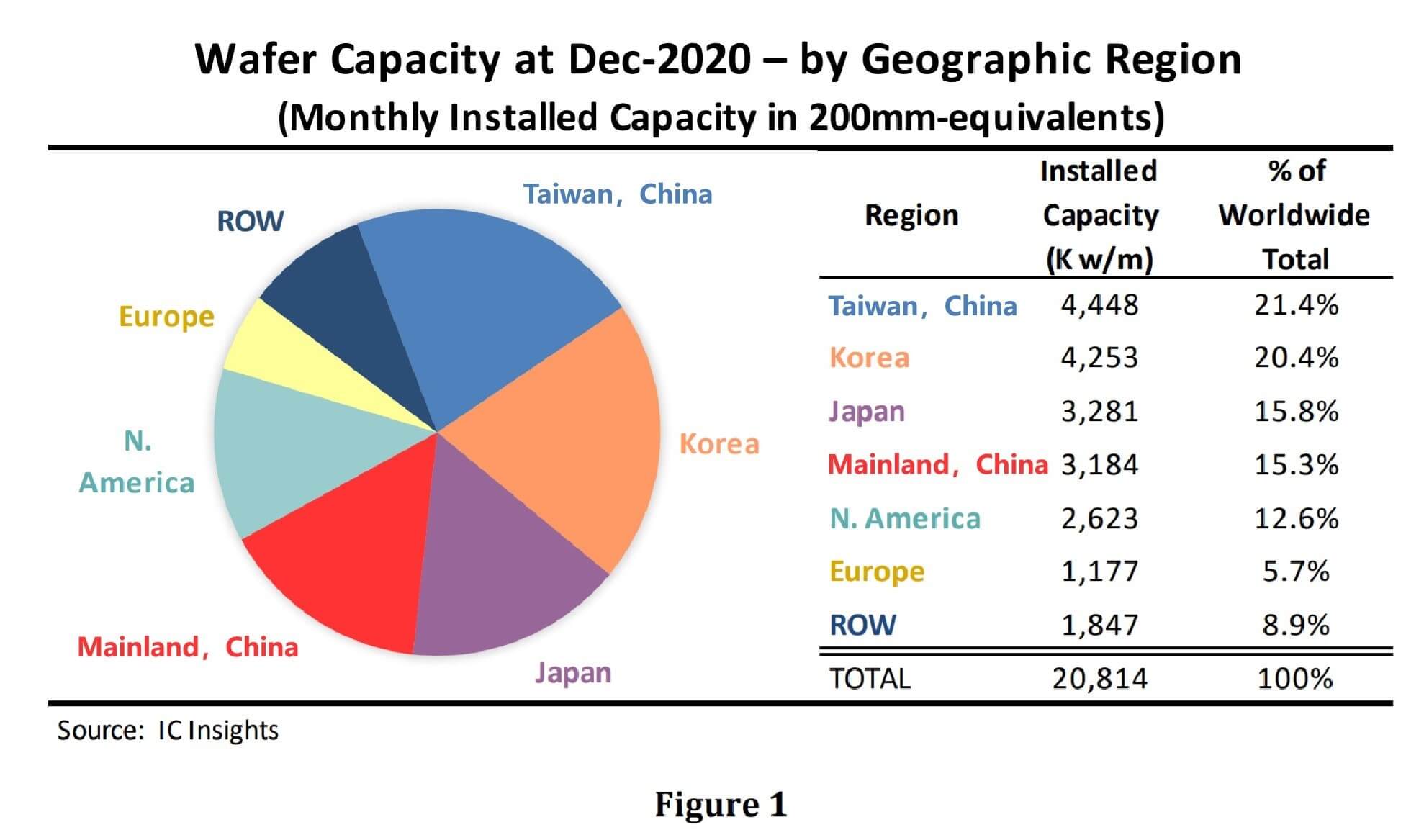

IC Insights released the latest report yesterday, which lists the global installed monthly wafer capacity from 2021 to 2025 by geographic region. Figure 1 shows the installed capacity by region as of December of 2020. The ROW “region” consists primarily of Singapore, Israel, and Malaysia, but also includes countries/regions such as Russia, Belarus, and Australia.

According to the report, as of December 2020, Taiwan region ranked first in the world with 21.4% of global wafer production capacity. South Korea ranks second, accounting for 20.4% of global wafer production capacity. Taiwan was the capacity leader at 200mm wafers. For 300mm wafers, South Korea was at the forefront followed closely by Taiwan. Samsung and SK Hynix continue to aggressively expand their fabs in South Korea to support their high-volume DRAM and NAND flash businesses.

IC Insights pointed out that Taiwan region surpassed South Korea in 2015 to become the largest capacity holder after having passed Japan in 2011. Taiwan is expected to remain the largest region for wafer capacity through 2025. The country is forecast to add nearly 1.4 million wafers (200mm-equivalent) in monthly fab capacity between 2020 and 2025.

At the end of 2020, mainland China held 15.3% of the world’s capacity, which was nearly the same as Japan. It is expected that China will surpass Japan in 2021 in terms of the amount of installed capacity. China accounted for more wafer capacity than Europe for the first time in 2010, it exceeded the capacity of the ROW region for the first time in 2016, and then it surpassed North America capacity for the first time in 2019.

The report stated that China is forecast to be the only region that gains percentage points of capacity share from 2020 to 2025 (3.7 percentage points). While expectations have been tempered for the roll out of the large new Chinese-led DRAM and NAND fabs, there is also a substantial amount of wafer capacity coming to China over the next few years from memory manufacturers headquartered in other countries and from local IC manufacturers.

The share of capacity in North America is projected to decline over the forecast period as the region’s large fabless supplier industry continues to rely on foundries, primarily those based in Taiwan region. Europe’s share of capacity is also expected to continue slowly shrinking.